The option to pay by credit card is no longer a convenience, but an expectation for many consumers. Some businesses now have signs reading “Card only” or “No cash/checks accepted.” The United States Mint even discontinued the penny last month, which many interpret as a sign of acceleration towards a cashless model. For law firms, this shift means clients expect the same convenience from a legal professional as from any other retail or service provider. The question is no longer whether to accept credit cards, but how to do it wisely.

Yet law firms still hesitate for an increasingly common reason: surcharges. If the surcharge ranges from 2-4% per transaction plus an additional subscription fee for the service, accepting credit cards can feel like a tough financial pill for many law firms to swallow. But the real financial downside isn’t the surcharge. It’s the unpaid invoice. And that is where the financial impact becomes clear. This article explains how to think about surcharges and how to absorb them without losing money.

Not Passing Surcharges on to Clients

Because credit card surcharges can add up quickly, many firms understandably wonder whether they can pass the surcharge on to the client. Oregon State Bar Formal Ethics Opinion 2005-172 addresses this issue briefly. The opinion notes that determining whether surcharges can be passed along to clients requires interpreting certain federal and state laws — a level of analysis beyond the scope of the opinion. However, it highlights that passing surcharges on to clients may implicate Regulation Z of the Truth in Lending Act (12 CFR pt 226), which would require you to make specific disclosures and offer cash discounts to clients if surcharges were imposed. Based on this guidance, it is advisable that you treat surcharges as a business expense rather than pass them on to clients. Even when you absorb the surcharges, offering credit card payments often results in collecting more of what you’re owed, which ultimately makes you more money. Absorbing these costs may feel counterintuitive, but doing so can actually lead to faster, more consistent payments, and improved cash flow.

Absorbing Surcharges Without Losing Money

Why, then, does absorbing surcharges often pay off? Clients are more willing to pay by credit card, and this willingness often outweighs the cost of the surcharge. A variety of reasons for this willingness exist. Many clients simply don’t have the cash available to pay their invoice immediately. Payment by credit card also removes most of the barriers that come with payment by check. Instead of writing a check and mailing or dropping it off at your office, clients can easily pay by credit card through a variety of methods, including a link or client portal. Let’s run the numbers to show how the surcharge often pays for itself. Imagine that you bill 20 clients at $1,000 each. Your surcharge for accepting credit cards is 2% per transaction.

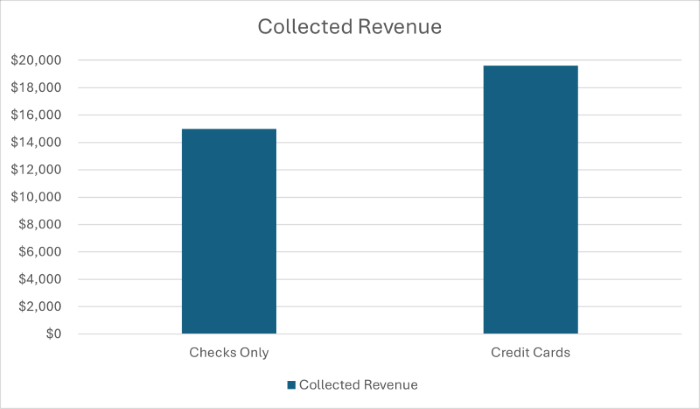

Scenario 1: You only accept checks (no surcharge). Let’s assume 15 out of 20 clients pay their invoice. Fifteen clients × $1,000 = $15,000 collected. With no surcharges, the total collected is $15,000. Even though you avoided the 2% surcharge, you lost $5,000 in uncollected revenue.

Scenario 2: You accept credit cards (2% surcharge). Clients appreciate the convenience, so all 20 clients pay. Twenty clients × $1,000 = $20,000 collected. If you add a 2% surcharge on each of the 20 payments, you are covering $20 per payment ($20 × 20 = $400 in surcharges). This means the total collected is $19,600. You paid $400 in surcharges but collected $4,600 more than in Scenario 1 (checks only).

By accepting credit cards, you net $4,600 more even after surcharges:

This example represents a 30% increase in actual money in the door. Firms can miss this because they picture the surcharge in isolation. The surcharge isn’t the cost. The cost is the unpaid invoice. Many clients expect fast, simple, digital payment options. When you don’t offer those options, you potentially delay collection, increase the risk of non-payment, and create more administrative work for you or your staff. Once you see how easily the cost of the surcharge can be absorbed — and even offset by receiving payments faster — the next step is to make paying by credit card as simple as possible for your clients. Doing so ensures you maximize the benefits of accepting credit cards.

How to Make it Easy for Clients to Pay Using a Credit Card

Your goal is simple: to get paid faster and more reliably by making it easy for clients to pay with a credit card. The most effective way to do that is to offer multiple, convenient credit card payment options. By removing friction in the payment process, you increase the likelihood that clients will pay promptly—and your firm will see improved cash flow. Here are the options firms should offer to streamline credit card payments:

- Accept payments by phone. Allow clients to call and pay by credit card over the phone. Some prefer this because speaking to a real person provides reassurance that the payment has been processed correctly, avoids concerns about online security, and can be quicker than logging in or searching for a payment link.

- Allow clients to pay via email, text message, or client portal. Offering multiple options lets clients choose the method that works best for them. Also be sure to use a legal credit card processing program. These programs let you run credit cards securely from various mobile devices, and they automatically withdraw the surcharge from your operating account, so you don’t have to put your own money into your trust account to cover it. Most practice management software programs, including Clio, 8amMyCase, and Smokeball, allow you to send invoices by email, text message, or through a client portal, all with a secure payment link. Standalone programs like LawPay or LexCharge offer these same features and integrate with many practice management programs.

- Provide a QR code on the invoice. QR codes allow clients to pay invoices directly from their mobile device. Upon scanning the code, they will be redirected to the payment page where they can see the invoice, enter their credit card information, and submit payment instantly. Most practice management programs and standalone payment programs allow you to send a QR code.